Regional platforms and platforms for suppliers and customers

Next: Defence for the Social Media Platforms

In the previous segments we’ve discussed about the nature of global platforms that sit in the middle between suppliers and customers. These are dominant platforms types but not the only ones. Let’s discover a little bit about the nature of regional/local platforms and what platforms for suppliers or customers could be.

Regional/local platforms capturing expert knowledge

The previous types of platforms for content (video, music), commerce and community (social media) have all global nature. A single company can build one platform to cover the entire earth.

Some services are by their nature local or have a strong local component. For example, attorney services rely heavily on know-how of local legislation, business practices and past local rulings of various cases.

Many other services also require extensive local know-how. Investment advice requires following local companies closely, talking with their leaders and understanding the nature of the local economy, local practices and what types of political ambitions people in government have. Health services, especially communicating with patients and discussing options, requires speaking the local language and understanding the non-verbal cultural issues and religious beliefs in different age groups that people have.

It seems expert services as platform are hard to do from the outside. Some aspects are very general such as the technical platform. A web shop is a web shop after all. One can also think that a service dedicated to a single disease like diabetes could well work globally as long as there is also a set of local doctors discussing results and options with patients.

The expert service needs a few add-ons to the generic platform model. Experts need to manage their calendar and facilities need to be managed. There needs to be contracts and integrations with the parties that own and operate the facilities like medical centers or office hotels.

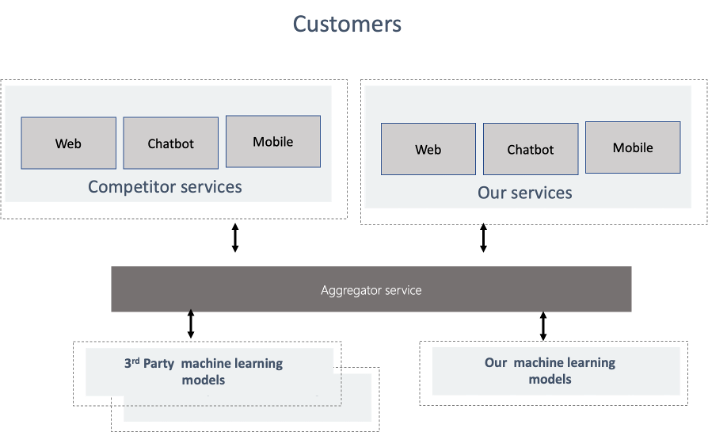

Even when expert services are very localised, large parts of them can be automated. The image below describes the main parts of an expert platform

Since expert service encapsulate a large body of knowledge, you cannot jump right into automating it immediately but an iterative approach is needed.

A typical approach is to start an online service where all requests are handled by human experts. Over time a database of cases, actions and results starts forming. Once there is enough material, machine learning can be applied. First to quickly surface relevant similar cases to the human expert as support. This can later be extended to provide possible recommendations to experts. Based on how the experts respond to advice, do they take it or select alternate action, the models learn slowly to work better. They start to learn.

Over time the models become better and better and at some time the company can think of offering a completely automated service at a radically different price. For example, for free to anyone. The free part can be time limited or limited to certain common conditions. This could be a marketing tool to bring in more customers, riding on the fact that automatisation can only go so far and a portion of users will purchase for-fee expert services later to better cope with their need.

Once such a model is working well, the expert service company can think of offering it to their direct competitors as an independent service. Why would anyone do that?

If the rake is small enough, this is a strong disincentive for anyone to start creating a competing automated expert service as a good option is already available. Building such a service and database of cases is expensive and full of risks.

The company offering the service to competitors in turn gets further cases to their database making the online service increasingly good and hard to replicate at the same time bringing in revenue.

This can only delay the inevitable as at later stages there will be multiple competing expert services for any area. It is human nature that other companies and startups want to compete, even when there is no business case. It’s the Not-Invented-Here (NIH) syndrome.

When there are multiple similar automated expert services, a new type of expert service company can emerge – the aggregator. The aggregator sources result from multiple underlying expert services. If these services have truly independent baselines for their models, the aggregator service tends to work better than any of the underlying service, but care has to be taken that their models are independently built from non-overlapping data. In AI same data means same information.

Platforms for suppliers and customers

Today’s platforms are trusted intermediaries between buyers and sellers. Nothing prevents the creation of separate platforms sellers and buyers – the ‘endpoints’. These have not become such important factors so far.

A supply (seller) platform would collect a large body of manufacturers/service providers and use its bargaining power to gain more favorable terms from the big orchestrator platforms. For vendors the needs are:

Gain better visibility into who the customers are

Reduce middle-platforms rake of the deal (lowers own costs)

In addition to working with a single platform, a supply platform can perform all kinds of useful analysis from different platforms and share the insights with its members.

As example people can join many work-related platforms for different activities – drive car, do some web design, draw, translate between English and my native language and so on. A supply platform for individual ‘gig’ workers can look at the many platforms and start analyzing them. What platforms require most unpaid work (like completing skill evaluations, wasting my time), where do I get information on market development, what types of platforms fetch best rates for a type of work and what categories of work bring highest pay, where do rates swing most, what category is over-competitive?

Next, they can look at my competences and start giving advice: what additional skills would I need to qualify for markedly better paying jobs – what courses to take or where to get needed on-the-job training.

Supply platforms have much better bargaining power than individual enterprises or people. They can withdraw all participating suppliers instantaneously if better terms are not achieved. To some degree this happens already today. On some airports ride-offering drivers tend to switch off their apps at the same time when price is too low. This leads to shortage of supply. Dynamic pricing jacks prices up so that when they all switch on later, everyone gets better rate for their drive.

Demand (purchase) platforms collect a large body of potential buyers and negotiate decrease in price due to volume effect. For a demand platform it makes sense to buy directly from manufacturers and omit layers in the middle for many categories. A demand platform might still make a contract with general orchestrator to get some small discount on all items if it represents a big enough purchasing power. Getting say 10-15% of for everything for your entire life will have an impact.

The dynamics will be interesting to follow when there are orchestrators on all three layers. Everyone doing dynamic pricing and trying to outsmart each other. It’s the three-body problem. You can get an approximation of how this could work by having two voice assistants at home and telling one to switch on the lights and another to switch them off.

A high-level view of the system is in the diagram below:

In the final part we try to build a defence case for centralised social media platforms that we’ve been bashing a little bit so far.